As the year draws to a close, the U.S. dollar has capped off its worst annual performance since 2017, with the U.S. Dollar Index (DXY) shedding approximately 9.5–10% to hover around 98. What began as a resilient powerhouse currency—buoyed by years of post-pandemic strength—unraveled dramatically, especially in the first half of the year when it posted its sharpest drop since the early 1970s.

This wasn’t just a quiet fade; it was a seismic shift that reshaped global trade, boosted U.S. exporters, stung American travelers abroad, and sparked heated debates about America’s economic trajectory under President Trump’s second term. Let’s dive into the forces behind this historic weakness.

The U.S. Dollar Index (DXY) charted a steep decline throughout 2025, reflecting a confluence of policy shocks and shifting investor sentiment.

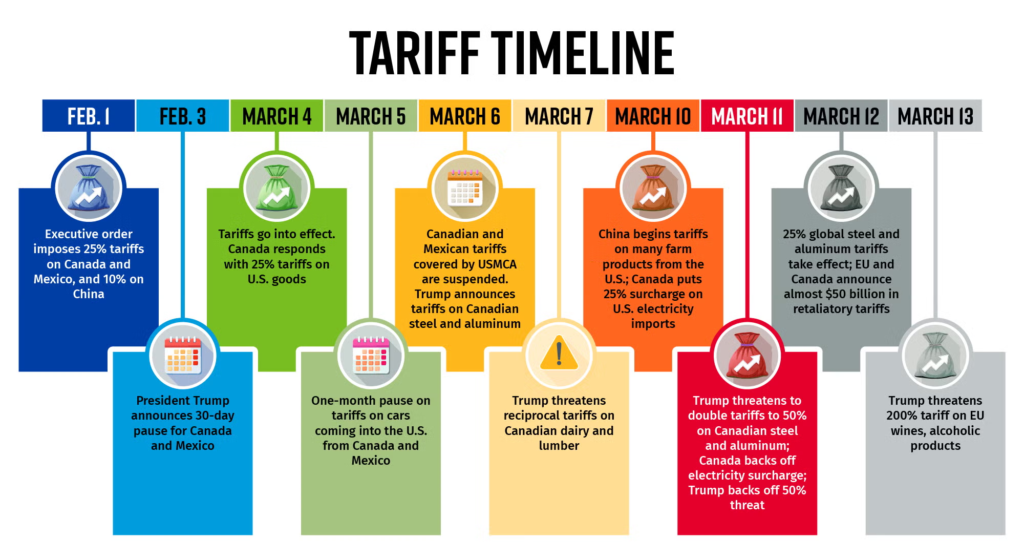

1. Tariff Turbulence: The Unexpected Backfire

Perhaps the biggest plot twist of 2025 was President Trump’s aggressive tariff agenda. Campaign promises of sweeping levies on imports—aimed at reviving American manufacturing and shrinking trade deficits—were rolled out with gusto, including broad tariffs on allies and adversaries alike.

Conventional wisdom held that tariffs would strengthen the dollar by curbing imports and reducing demand for foreign currencies. But reality proved messier. The sheer scale and unpredictability of the policies spooked markets, raising fears of slower U.S. growth, higher inflation, and potential recession. Investors fled dollar-denominated assets, viewing the chaos as a threat to America’s economic stability.

In the first half of the year, announcements triggered sharp sell-offs, with the dollar plunging over 10% by mid-year. Even as some tariffs generated record revenue (helping trim the fiscal deficit slightly), the uncertainty eroded confidence in U.S. assets as a “safe haven.”

Trump’s “Liberation Day” tariff rollout symbolized a bold but disruptive shift, contributing to market volatility and dollar pressure.

2. Federal Reserve Rate Cuts: Closing the Interest Gap

A classic driver of currency strength is interest rate differentials. For years, higher U.S. rates attracted global capital, propping up the dollar. But in 2025, the Fed delivered multiple cuts—three in the latter part of the year—amid signs of cooling inflation and a softening labor market.

As U.S. rates converged with (or fell below) those in peer economies, the dollar’s yield advantage evaporated. Markets priced in further easing into 2026, accelerating the greenback’s decline. Foreign investors, holding trillions in U.S. assets, began hedging their exposure—effectively selling dollars and amplifying the downturn.

3. Fiscal Fears and Policy Uncertainty

America’s ballooning deficits and debt didn’t help. Despite tariff revenues providing a modest boost, the fiscal 2025 deficit clocked in around $1.8 trillion. Concerns over unsustainable borrowing, coupled with headlines about potential Fed independence threats and erratic policy shifts, chipped away at the dollar’s perceived reliability.

Global investors reassessed their heavy bets on U.S. assets, prompting capital rebalancing toward Europe and elsewhere. This “de-dollarization” whisper grew louder, even if the dollar’s reserve status remained intact.

4. The Winners: Euro, Pound, and Beyond

The dollar’s pain was others’ gain. The euro surged over 13% against the greenback—the most since the financial crisis—fueled by relative European stability and fiscal support in Germany. The British pound climbed about 7.5–8%, while even emerging market currencies benefited.

The Japanese yen was a notable exception, staying muted due to the Bank of Japan’s cautious tightening. But overall, the shift marked a rare broad-based dollar retreat.

What It Meant for Everyday Americans and the World

A weaker dollar had silver linings: U.S. exports boomed (up 5% in the first nine months), corporate earnings got a tailwind, and foreign tourists flocked to cheaper U.S. destinations. President Trump himself highlighted these benefits, arguing a softer greenback helps “make a hell of a lot more money.”

But there were downsides too. Imported goods grew pricier, fueling inflation risks and hitting consumers’ wallets—think costlier European vacations or electronics. For investors, it reshaped portfolios, favoring international stocks and commodities.

Looking Ahead: More Weakness in 2026?

As 2025 ends, analysts largely expect modest further declines, with lingering tariff effects, Fed easing, and fiscal pressures in play. Yet the dollar’s dominance endures—no viable alternative has emerged.

This year’s slide wasn’t the end of the dollar era, but a stark reminder: even the world’s reserve currency isn’t invincible when policy storms hit. In a year of surprises, the greenback’s humbling served as a cautionary tale for global finance.